If there is something absolutely true on theses days, is the global economy is going through an episode to be treated by macroeconomists, analysts or historians. The economic history will talk about these current times in the future, as it is already talking about other historical chapters, such as 1929 crisis, great depression, 1973 crisis or the soviet empire fallen in 1989.

Historical Background

It seems like the global economy is not the same since Lehman Brothers collapsed on 15th of September of 2008 and subsequently AIG bankrupcy two weeks later through CDS (Credit default swaps) issued to back up CDO's (Collateral debt obligations) launched by US Investment banks worldwide, hiding NINJA mortgages in those, which generated the famous "subprime crisis". This is the origin of global crisis as we know it. Crisis which has come through different phases in the last 7 years. From subprime crisis to housing bubbles burst, banking system downfall, banking capitalisation from Governments public expenditure, european public deficits issues, government bonds crisis through enormous borrowing rates on the Eurozone, austerity schemes imposed through fiscal policies (slashing public expenditure and increasing taxes), european bail-outs on Portugal, Ireland, Spain or Greece (three times already), deflation exposure and more austerity. All those austerity schemes in Eurozone have had a strong impact on the global economy.

European austerity and international impact

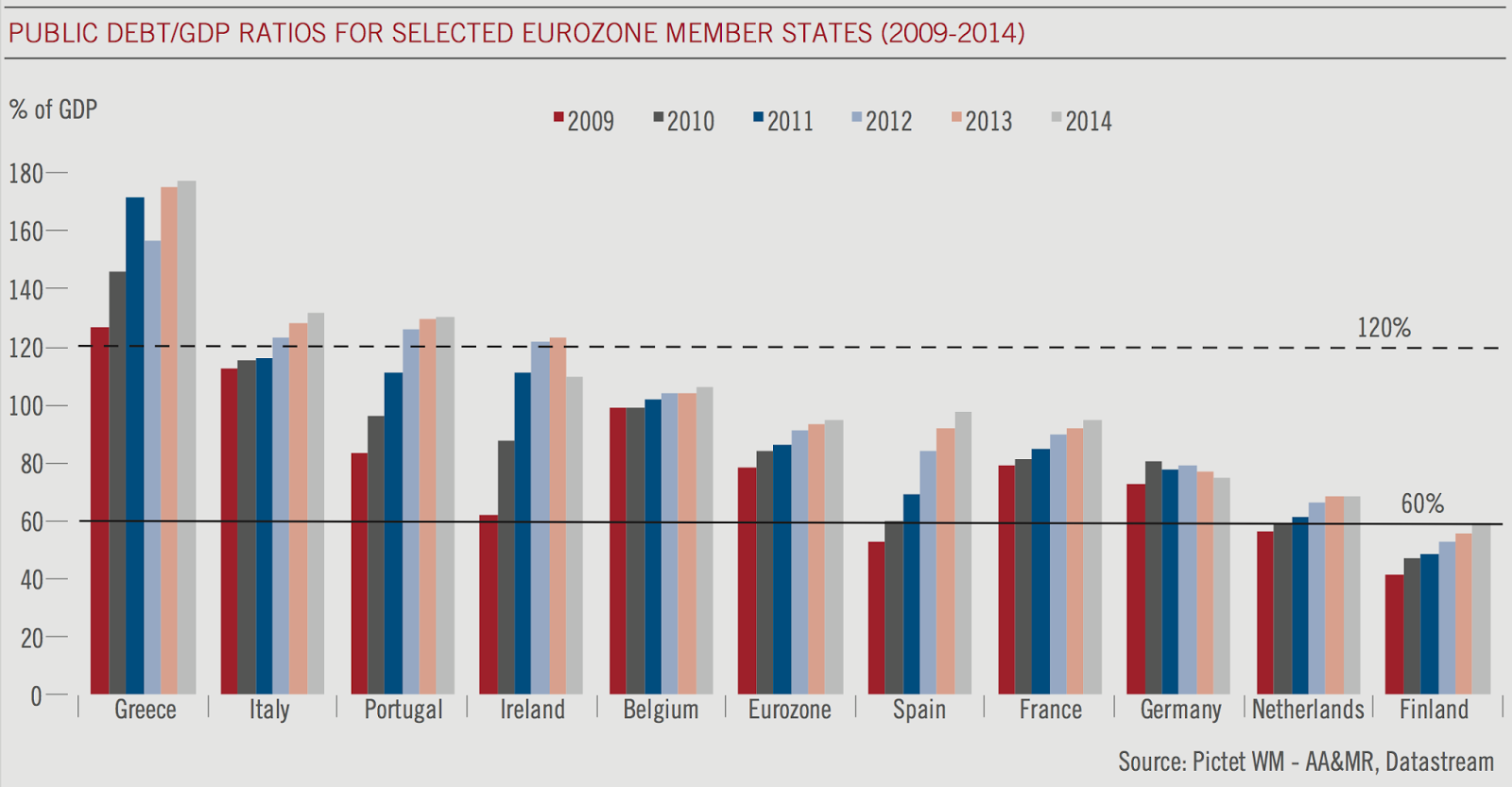

When any eurozone state applies any restrictive fiscal policy to meet Eurozone requirements in terms of public deficit (by 3%) and debt to GDP ratio (by 60%), the internal demand on those countries is seriously damaged, (not to mention the social dimension of this affair) and going through a deflation spiral, what impacts negatively on Eurozone economy imports and international trading accordingly. The imports from ones, are the exports from the others, as simple as that. It is interesting to see how the wealthier countries in the eurozone like Germany, impose austerity to south european countries, when none of them fulfil 60% Debt/GDP target. See chart below

That's why USA and China, for example, have seen as their economic growth have performed lower than expected in the last years. The European austerity has impacted on other countries. In global economy is all about strategy and games theory. Therefore, any action from ones may be followed by reaction from the others.

Chinese Yuan devaluation

China, whose economic growth has performed over 7% in terms of GDP (quite far from two digits-economy growth from the last decade) has decided to enhance its economic growth driven by Chinese exports. In response to European austerity.Therefore, Central Bank of China has made the decision to devaluate "Yuan" (Chinese currency) three times in three days (August 2015). It has been an earthquake on the economy worldwide, which has brought consequences such as:

However, US Dollar and other currencies have become in a "shelter currency" bearing in mind currencies devaluation worldwide, as load of investors are putting their capital and equities in wealthier economies, and running away from devaluated ones.

Just see the impact on Global currencies from Yuan devaluation on the chart below.

Oil Prices downfall and USA fracking.

On the other hand, oil prices have come down dramatically, due to Fracking oil and oil shale production in USA and other countries, what is providing a strong independence from oil imports and an increase on oil supply globally, as Saudi Arabia (main producer) has kept up the production to beat down oils prices overall. (over 50$/barrel) and be able to compete with prices from non-conventional oil production in USA.

Winners, oil importers. Losers, oil exporters. (See chart below).

This price reduction has stronger negative impact on OPEP countries where 90% of their incomes come from oil production like Nigeria, Venezuela, Ecuador and Angola. However, Saudi Arabia which production cost per barrel is over 5$, has margin enough to reduce prices and trying to dismantle oil fracking production in USA (It is well known, some fracking production areas in USA are waiting for oil prices to mark up to 60$ or 70$/barrel, as they start being profitable over those rates). Finally, Iran will launch oil production after getting off its "embargo" with USA, what will lead a oil production prices even lower.

Japan. Chronic economic stagnation

Finally, the Japanese impact on the global economy. Japan is the third biggest economy in the world, and remains on economic stagnation throughout two decades already. Neither monetary policy, nor fiscal policy stimulus have helped out to taking off from this "Status Quo". The main characteristic on its macroeconomy is the external debt accrued. It represents 230% of GDP. The highest ratio in the world (See chart below). Debt won't be probably reimbursed. Some analysis performed show the primary deficit to GDP in Japan (public deficit disregarding financial expenses from the external debt) should be over 5.4% (positive - surplus) in 2020, rather than the current 6% (negative- deficit) and keep it up of the whole next decade to repay debt obligations in 2030 easily. The only way to do so, should be through restrictive fiscal policy, increasing taxes and cutting public expenditure, what will lead further deflation and economic downturn. Well, the fiscal crisis in Japan is just around the corner.

On the other hand, Japanese monetary policy. Interest rates in Japan had come through rates close to 0% in the last two decades (over 0.10% currently) and fiscal policy stimulus like investing in public infrastructures and cutting taxes. Measurements to enhance an economic growth, that never comes over. It is basically "the liquidity trap" already exposed by John Maynard Keynes nearly one century ago. Nothing new.

Also, Japanese "quantitive easing" applied by Bank of Japan to finance their public deficit and keep borrowing rates down to 0.33% (10 year-bond-rate) is devaluating Japanese Yen.

Finally, Chinese economic downturn has reduced Japanese exports by 4.4% and a reduction on internal consumption (that represent 60% of Japanese GDP), have produced 1.6% GDP fallen in Q2 - 2015.

This is the current global economy, debt issues, bail-outs, currency devaluations, deflation, oil and commodities prices slump, stagnation, austerity.....what else?.....place your bets!!

Historical Background

It seems like the global economy is not the same since Lehman Brothers collapsed on 15th of September of 2008 and subsequently AIG bankrupcy two weeks later through CDS (Credit default swaps) issued to back up CDO's (Collateral debt obligations) launched by US Investment banks worldwide, hiding NINJA mortgages in those, which generated the famous "subprime crisis". This is the origin of global crisis as we know it. Crisis which has come through different phases in the last 7 years. From subprime crisis to housing bubbles burst, banking system downfall, banking capitalisation from Governments public expenditure, european public deficits issues, government bonds crisis through enormous borrowing rates on the Eurozone, austerity schemes imposed through fiscal policies (slashing public expenditure and increasing taxes), european bail-outs on Portugal, Ireland, Spain or Greece (three times already), deflation exposure and more austerity. All those austerity schemes in Eurozone have had a strong impact on the global economy.

European austerity and international impact

When any eurozone state applies any restrictive fiscal policy to meet Eurozone requirements in terms of public deficit (by 3%) and debt to GDP ratio (by 60%), the internal demand on those countries is seriously damaged, (not to mention the social dimension of this affair) and going through a deflation spiral, what impacts negatively on Eurozone economy imports and international trading accordingly. The imports from ones, are the exports from the others, as simple as that. It is interesting to see how the wealthier countries in the eurozone like Germany, impose austerity to south european countries, when none of them fulfil 60% Debt/GDP target. See chart below

That's why USA and China, for example, have seen as their economic growth have performed lower than expected in the last years. The European austerity has impacted on other countries. In global economy is all about strategy and games theory. Therefore, any action from ones may be followed by reaction from the others.

Chinese Yuan devaluation

China, whose economic growth has performed over 7% in terms of GDP (quite far from two digits-economy growth from the last decade) has decided to enhance its economic growth driven by Chinese exports. In response to European austerity.Therefore, Central Bank of China has made the decision to devaluate "Yuan" (Chinese currency) three times in three days (August 2015). It has been an earthquake on the economy worldwide, which has brought consequences such as:

- Decapitalisation on Chinese economy. Massive capital and equities flow out of China and heading for appreciated currency-economies, like USA, after currency devaluation took place. China has on of the most currency reserves in the world. However, the last report shows capital outflows for 96,000 mill ($) setting down the total currencies reserves to 3.6 bn($), as well as the Chinese government had to spend over 200.000 mill ($) to avoid further devaluations.

- Commodities prices slump, impacting negatively on emerging economies, . which are China's suppliers. This devaluation raise imports prices from countries suppliers and reduce the global demand, what set commodities prices down. Special mention to Brazil that comes into technical recession though GDP reduction by 1.6% afterward.

- Currency devaluation on emerging economies like Indonesia, Malaysia, Vietnam or Brazil, in oder to maintain a competitive approach to their main client (China). On the other hand, some of those emerging economies got external debt in US dollars, which has increased their leverage, due to a stronger US dollar.

- Janet Yellen (FED's president) has not raised interest rate in USA, which is still over 0%. Interest rates strategy from FED depends on Inflation (by 2%) and unemployment targets (by 7%). Current inflation rate in USA is 0.2% and unemployment by 5.1%. Potentially, an increase on interest rates would lead an US Dollar appreciation (already strong enough) what would enhance imports from China impacting negatively on US employment.

However, US Dollar and other currencies have become in a "shelter currency" bearing in mind currencies devaluation worldwide, as load of investors are putting their capital and equities in wealthier economies, and running away from devaluated ones.

Just see the impact on Global currencies from Yuan devaluation on the chart below.

Oil Prices downfall and USA fracking.

On the other hand, oil prices have come down dramatically, due to Fracking oil and oil shale production in USA and other countries, what is providing a strong independence from oil imports and an increase on oil supply globally, as Saudi Arabia (main producer) has kept up the production to beat down oils prices overall. (over 50$/barrel) and be able to compete with prices from non-conventional oil production in USA.

Winners, oil importers. Losers, oil exporters. (See chart below).

This price reduction has stronger negative impact on OPEP countries where 90% of their incomes come from oil production like Nigeria, Venezuela, Ecuador and Angola. However, Saudi Arabia which production cost per barrel is over 5$, has margin enough to reduce prices and trying to dismantle oil fracking production in USA (It is well known, some fracking production areas in USA are waiting for oil prices to mark up to 60$ or 70$/barrel, as they start being profitable over those rates). Finally, Iran will launch oil production after getting off its "embargo" with USA, what will lead a oil production prices even lower.

Japan. Chronic economic stagnation

Finally, the Japanese impact on the global economy. Japan is the third biggest economy in the world, and remains on economic stagnation throughout two decades already. Neither monetary policy, nor fiscal policy stimulus have helped out to taking off from this "Status Quo". The main characteristic on its macroeconomy is the external debt accrued. It represents 230% of GDP. The highest ratio in the world (See chart below). Debt won't be probably reimbursed. Some analysis performed show the primary deficit to GDP in Japan (public deficit disregarding financial expenses from the external debt) should be over 5.4% (positive - surplus) in 2020, rather than the current 6% (negative- deficit) and keep it up of the whole next decade to repay debt obligations in 2030 easily. The only way to do so, should be through restrictive fiscal policy, increasing taxes and cutting public expenditure, what will lead further deflation and economic downturn. Well, the fiscal crisis in Japan is just around the corner.

On the other hand, Japanese monetary policy. Interest rates in Japan had come through rates close to 0% in the last two decades (over 0.10% currently) and fiscal policy stimulus like investing in public infrastructures and cutting taxes. Measurements to enhance an economic growth, that never comes over. It is basically "the liquidity trap" already exposed by John Maynard Keynes nearly one century ago. Nothing new.

Also, Japanese "quantitive easing" applied by Bank of Japan to finance their public deficit and keep borrowing rates down to 0.33% (10 year-bond-rate) is devaluating Japanese Yen.

Finally, Chinese economic downturn has reduced Japanese exports by 4.4% and a reduction on internal consumption (that represent 60% of Japanese GDP), have produced 1.6% GDP fallen in Q2 - 2015.

This is the current global economy, debt issues, bail-outs, currency devaluations, deflation, oil and commodities prices slump, stagnation, austerity.....what else?.....place your bets!!